Insurance Product Filing in the United States: Process, Challenges, and the Role of System Intelligence in Accelerating Regulatory Approval

Introduction

Insurance product filing in the United States is one of the most structured and heavily regulated processes in the financial services industry. Every new insurance product or modification to an existing product must pass through a rigorous, multi-layered review process governed primarily at the state level. While this system is designed to protect consumers and ensure market stability, it also introduces complexity, delay, and operational overhead for carriers.

The introduction of system intelligence testing has begun to reshape how carriers approach filings. By embedding automation, validation logic, and predictive analytics into the product development lifecycle, carriers are now able to significantly reduce filing errors, accelerate approval cycles, and improve regulatory alignment.

This blog post explores the end-to-end insurance product filing process in the United States, the challenges inherent in multi-jurisdictional compliance, and how system intelligence is transforming the speed and accuracy of regulatory submissions.

Understanding Insurance Product Filing in the United States

Insurance product filing refers to the formal submission of insurance policy forms, rates, actuarial justifications, and supporting documentation to state insurance regulators for approval. In the United States, insurance regulation is not centralized at the federal level. Instead, each state maintains its own insurance department with its own regulatory framework, filing requirements, and review timelines.

This decentralized structure means that a single insurance product intended for national distribution may require dozens of separate filings, each tailored to the specific rules of individual states. These variations can include differences in required policy language, rating methodologies, disclosure obligations, and consumer protection standards. At a high level, the filing process ensures that insurance products are fair, transparent, actuarially sound, and compliant with applicable laws before they are sold to consumers.

The Internal Product Development and Filing Preparation Phase

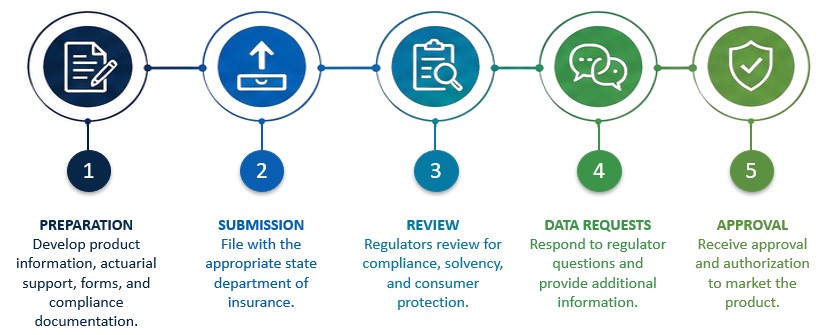

Before any filing is submitted to regulators, carriers go through a detailed internal development process. This begins with product design, where cross-functional teams collaborate to define coverage features, pricing structures, underwriting rules, and policy terms.

Actuarial teams are responsible for building pricing models and ensuring that rates are sufficient to cover expected claims while maintaining profitability. Legal and compliance teams review policy wording to ensure alignment with state regulations and consumer protection laws. Product and operations teams coordinate to ensure that the product can be operationalized within existing systems and distribution channels.

Once the product design is finalized, the filing preparation phase begins. This involves assembling a comprehensive package of documentation that typically includes policy forms, endorsements, actuarial memoranda, rate tables, and explanatory materials. One of the most critical aspects of this phase is ensuring internal consistency across all documents. Even minor discrepancies between policy language and actuarial justification can result in regulatory objections or delays.

Submission Through Regulatory Systems

After internal preparation and review, filings are submitted to state insurance departments through electronic systems such as SERFF, the System for Electronic Rate and Form Filing. These platforms serve as centralized hubs for submission, tracking, and communication between carriers and regulators.

Despite the efficiencies introduced by electronic filing systems, the submission process remains complex due to varying state specific requirements. Each jurisdiction may require different supporting documentation or interpret filing rules differently, which increases the administrative burden on carriers operating across multiple states. Once submitted, filings enter a queue for regulatory review, where state analysts evaluate the submission for compliance, accuracy, and consumer fairness.

Regulatory Review and Approval Process

During the regulatory review stage, state insurance departments conduct a detailed analysis of the filing. This includes reviewing policy language for clarity and compliance, evaluating actuarial assumptions for soundness, and ensuring that rates are not excessive, inadequate, or unfairly discriminatory.

Regulators may issue objections or requests for additional information, initiating a back-and-forth communication cycle between the carrier and the regulatory body. Each round of correspondence can extend the approval timeline significantly.

Different states also operate under different approval frameworks. Some require explicit approval before a product can be marketed, while others allow file-and-use or use-and-file mechanisms. These differences require carriers to carefully manage launch timing and jurisdictional rollout strategies.

Insurance Product Approval Timelines

One of the most common questions carriers ask during the filing process is how long it will take for a product to receive regulatory approval. The answer varies significantly depending on the product type, filing complexity, state jurisdiction, and the number of objections raised during review.

In general, straightforward rate or form changes may receive approval within 30 to 60 days in some states, particularly under file-and-use frameworks where products can be implemented shortly after submission. However, more complex filings such as new life insurance products, annuities, or products involving innovative underwriting or pricing structures can take several months to receive approval.

For national carriers filing across multiple jurisdictions, the timeline becomes even more challenging. Because each state operates independently, approvals do not occur simultaneously. Some states may approve a filing quickly, while others issue multiple rounds of objections or requests for clarification that extend the review cycle significantly. In practice, a nationwide rollout can often take anywhere from six months to more than a year depending on the complexity of the product and the responsiveness of the filing process.

Several factors commonly influence approval timelines:

- The completeness and accuracy of the initial filing package

- The clarity and consistency of policy language

- The complexity of actuarial assumptions and rate structures

- State specific regulatory requirements and review workloads

- The number of objection cycles between regulators and carriers

This is where system intelligence is having a measurable impact. By identifying inconsistencies and compliance risks before submission, intelligent validation systems help carriers reduce objection rates and shorten review cycles. Improving first pass filing quality not only accelerates approvals but also enables carriers to launch products faster and gain earlier access to market opportunities.

Key Challenges in the Insurance Filing Process

One of the most significant challenges in insurance product filing is regulatory variability across states. A filing that meets requirements in one jurisdiction may need substantial revision in another due to differences in statutory language or regulatory interpretation.

Another major challenge is the high volume of filings managed by large carriers. Organizations may submit hundreds or even thousands of filings annually, each requiring precise documentation, version control, and compliance validation. This creates a significant operational burden and increases the likelihood of human error.

Additionally, the filing process is still heavily reliant on manual review and coordination across multiple teams. This sequential workflow can create bottlenecks, slow down product launches, and increase the cost of compliance.

The Emergence of System Intelligence in Insurance

System intelligence refers to the use of advanced analytics, automation, and intelligent validation systems to enhance decision making and operational efficiency in complex workflows. In the context of insurance product filing, system intelligence is being used to streamline validation, reduce errors, and accelerate regulatory approval.

Rather than relying solely on manual review processes, carriers can now embed intelligence into the filing lifecycle to detect inconsistencies, validate compliance, and simulate regulatory outcomes before submission. This shift represents a fundamental change in how filings are prepared and reviewed, moving from reactive correction to proactive prevention.

Pre-Filing Validation and Error Detection

One of the most impactful applications of system intelligence is pre-filing validation. Before a filing is submitted to regulators, intelligent systems can analyze policy forms to identify inconsistencies or compliance risks. This includes detecting mismatches in numerical values. By identifying issues early, carriers can reduce the likelihood of regulatory objections and avoid costly rework cycles.

Ensuring Consistency Across Filing Components

Insurance filings involve multiple interconnected documents, and consistency across these documents is critical. System intelligence tools can automatically compare data points across policy forms to ensure alignment. This reduces the risk of discrepancies that might otherwise go unnoticed during manual review. It also improves the overall quality and integrity of the filing package, increasing the likelihood of first-pass approval.

Business Impact: Speed, Cost, and Market Advantage

The adoption of system intelligence in insurance product filing has significant business implications. Faster validation and reduced rework lead to shorter approval cycles, enabling carriers to bring products to market more quickly.

This speed advantage is particularly important in competitive markets where timing can directly impact revenue and market share. Additionally, automation reduces the need for extensive manual review, lowering operational costs and improving resource efficiency.

The Evolution of Compliance as a Continuous Process

System intelligence is also driving a shift in how carriers view compliance. Rather than treating filing as a final step in product development, compliance is becoming a continuous, embedded process throughout the product lifecycle. This means that regulatory alignment is maintained in real time, rather than being validated only at the point of submission. As a result, carriers are better prepared to adapt to regulatory changes and market demands.

Final Thoughts

Insurance product filing in the United States remains a complex and highly regulated process shaped by state-level oversight, detailed documentation requirements, and evolving regulatory standards. While these safeguards are essential for consumer protection and market stability, they also introduce significant operational challenges for carriers.

System intelligence is emerging as a transformative force in this environment. By enabling automated validation and improving consistency, intelligent systems are fundamentally improving the efficiency and accuracy of the filing process. As the insurance industry continues to evolve, carriers that integrate system intelligence into their filing workflows will be better positioned to reduce friction, accelerate product launches, and maintain regulatory excellence in an increasingly complex landscape.

To read more about System Intelligence, Quality Assurance, QMT, QMT TruePDF, QMT TrueXML, and technology topics, visit our blog or visit our resource center. Try QMT TruePDF for free – click here. Book a demo here.

About the Author

Neil Bendov, MBA, is a VP of Marketing at Emtech. He is a seasoned marketing professional driven by a passion for cultivating brand success. With a diverse background and a track record of delivering results, Neil specializes in creating and executing innovative business-to-business marketing strategies that resonate with target audiences. Armed with a keen understanding of customer behavior and market trends, he has successfully navigated the dynamic landscape of digital and traditional marketing channels.